We’re not digging into another IPO filing today. You can read all about AppLovin’s filing here, or ThredUp’s document here.

This morning, instead, we’re talking about an old favorite: software valuations. The folks over at Battery Ventures have compiled a lengthy dive into the 2020 software market that’s worth our time — you can read along here; I’ll provide page numbers as we go — because it helps explain some software valuations.

The Exchange explores startups, markets and money. Read it every morning on Extra Crunch, or get The Exchange newsletter every Saturday.

There’s little doubt that there is some froth in the software market, but it may not be where you think it is.

The Battery report has a lot of data points that we’ll also work through in this week’s newsletter, but this morning, let’s narrow ourselves to thinking about rising aggregate software multiples, the breakdown of multiples expansion through the lens of relative growth rates, and cap it off with a nibble on the importance, or lack thereof, of cash flow margins for the valuation of high-growth software companies.

We’ll look at the changing public market perspective, and then ask ourselves if the aggregate image that appears is good or not good for software startups.

We’ll look at the changing public market perspective, and then ask ourselves if the aggregate image that appears is good or not good for software startups.

I chatted through pieces of the report with its authors, Battery’s Brandon Gleklen and Neeraj Agrawal. So, we’ll lean on their perspective a little as we go to help us move quickly. This is our Friday treat. Or at least mine. Let’s get into it.

Rising multiples

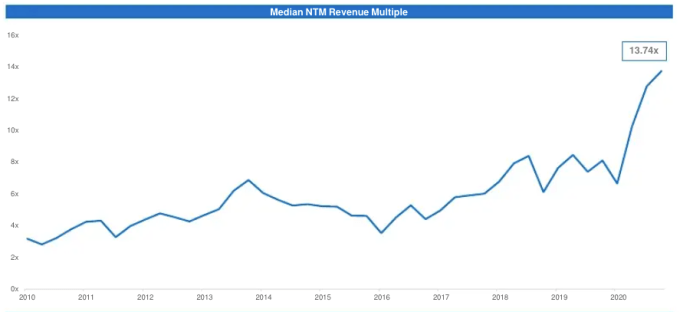

Let’s start with an affirmation. Yes, software valuations have risen to record-high multiples in recent years. Here’s the Battery chart that makes the change clear:

Page 31, Battery report

[ad_2]

Source link

{kind=link}